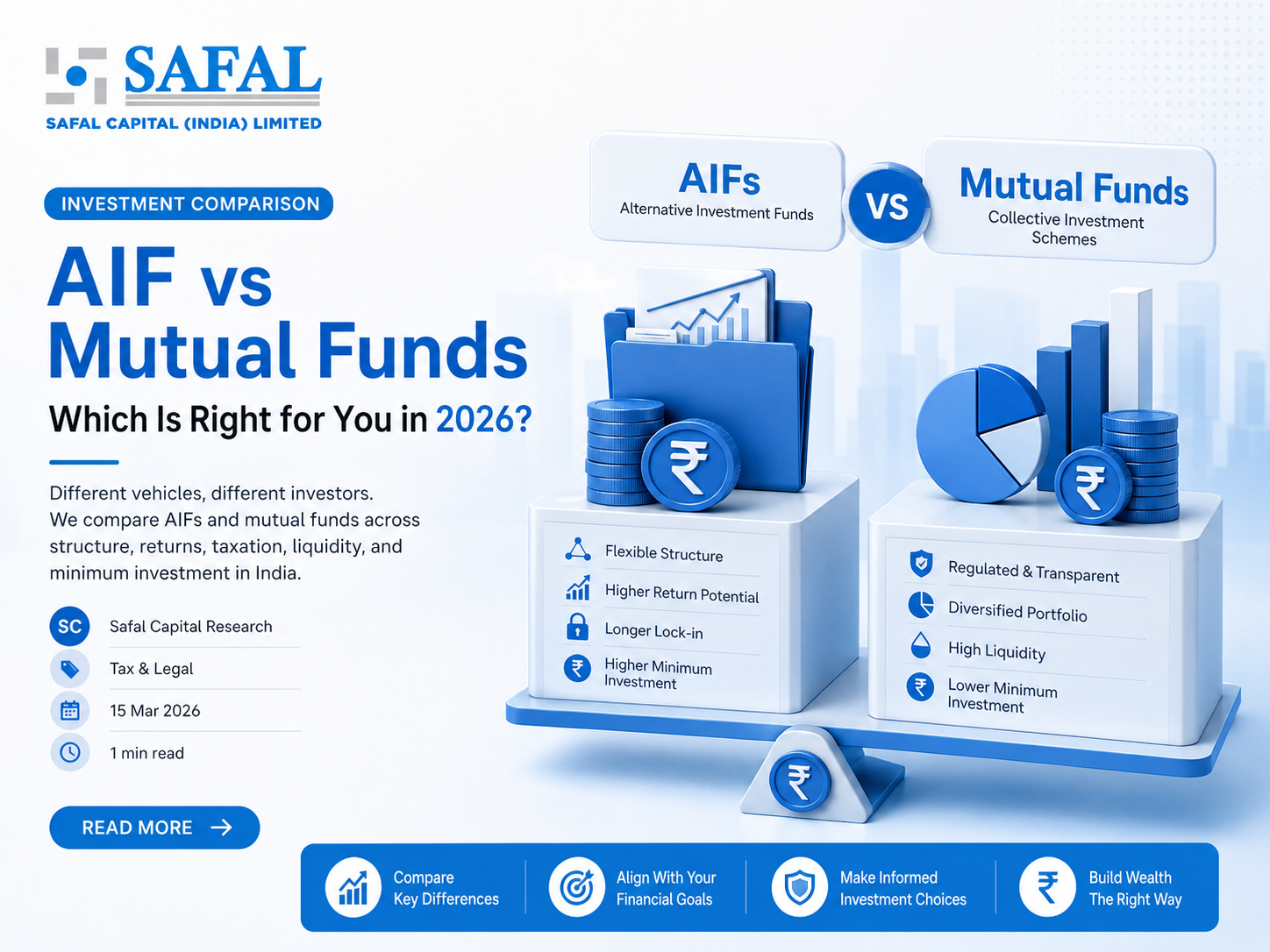

Structural Differences

Mutual funds are open-ended, daily-NAV products available to retail investors with minimums starting at ₹500. AIFs are closed-ended (Cat I & II) or open-ended hedge-style (Cat III), with a SEBI-mandated minimum of ₹1 crore per investor.

Mutual funds invest primarily in listed securities and follow strict diversification rules. AIFs can invest in unlisted equity, structured credit, real estate, and other private market assets, categories that mutual funds typically can't access.

Returns and Fees

Mutual fund expense ratios are tightly regulated. AIFs charge a management fee (typically 1.5–2% per annum) plus carried interest on returns above a hurdle rate (usually 8%).

- Mutual fund equity: Target 12–15% long-term, daily liquidity, ₹500 minimum.

- Cat II AIF: Target 18–22% IRR over 7 years, locked-in capital, ₹1 crore minimum.

- Cat III AIF: Target 15–20%, with leverage permitted, varying lock-ins.

Taxation

AIFs (Cat I and II) enjoy pass-through taxation, the fund itself is not taxed; investors pay tax on their share of gains as if they earned them directly. For HNIs in higher brackets, AIF taxation can be more efficient when underlying gains are long-term capital gains on unlisted securities.

Mutual funds are about access. AIFs are about access to the kind of opportunities mutual funds can't legally hold. Rajesh Mehta, Founder

Which One Is Right for You?

If you're building wealth through monthly contributions and value daily liquidity, mutual funds are almost certainly the better starting point. If you have ₹1 crore+ to commit and are comfortable with 5–7 year illiquidity, AIFs deserve a serious look as a satellite holding alongside a mutual fund core.